Digitization is a megatrend that has already transformed many industries – and now it’s banking’s turn. But digital banking is about more than just rebranding or adding a mobile app: it requires highly personalized transactions. In this sense, banks have a lot to learn from decentralized finance, or DeFI.

There are still lots of issues to solve before we can celebrate the coming of a new digital banking age:

- Customers of even the same bank can’t directly interact with each other;

- Cross-border transfers remain expensive and ridden with middlemen;

- Bank users can’t convert fiat into crypto and back; and

- New banking services take ages to develop, approve and introduce.

In DeFi, most of these problems have already been resolved. Users can lend each other money directly; earn more than 10% a year on crypto deposits; send money abroad in seconds, and much else. Banks could greatly benefit from these instruments. The problem is that developing a crypto-fiat DeFi platform from scratch is expensive and requires expertise that most banks’ IT teams simply don’t have.

Introducing Cryptoenter: a turn-key DeFi solution for banks

The way to solve this conundrum is to implement a versatile DeFi infrastructure that any bank could use out of the box. That’s exactly what Cryptoenter does: it’s a ready-to-use platform that facilitates interactions between banks and their users – as well as between users themselves, wherever they are in the world.

As soon as a financial institution integrates Cryptoenter, its customers gain access to dozens of DeFi services:

- P2P lending (users issue each other loans in crypto and fiat);

- Cryptocurrency/fiat wallet;

- Fiat-crypto and crypto-fiat gateways;

- Instant and cheap cross-border transfers (remittance fees don’t exceed $1);

- Real-time value exchange;

- Payment processing and acquiring;

- Crowdfunding and a social network for investors;

- Issuing stablecoins and new cryptocurrencies;

- Interbank payments, and much else.

Essentially Cryptoenter provides a virtual banking front end and a ready system for managing customers’ fiat and crypto accounts. As long as two banks sign up as validators on Cryptoenter, their customers can interact with each other in the same way as customers of the same bank. For the financial institution, the benefits are many:

- Extra revenue (charging fees on DeFi services);

- Increased customer loyalty;

- Expansion into new regions (branchless banking);

- Easy customer acquisition.

Scalable and easy to implement

Thanks to a handy API, Cryptoenter is quick and easy to integrate into the backend and frontend of any bank. Every end customer gets a personal crypto-fiat wallet and can start using DeFi services immediately through the familiar interface. Meanwhile, the bank itself can focus on marketing instead of spending money on product development.

To ensure scaling and speed, Cryptoenter leverages Linux Foundation’s Hyperledger Fabric – the first DeFi project to do so. The platform also uses Rubicon Blockchain by Smart Block Laboratory and a number of IBM solutions, including IBM Cloud, Kubernetes, and Cloud Object Storage.

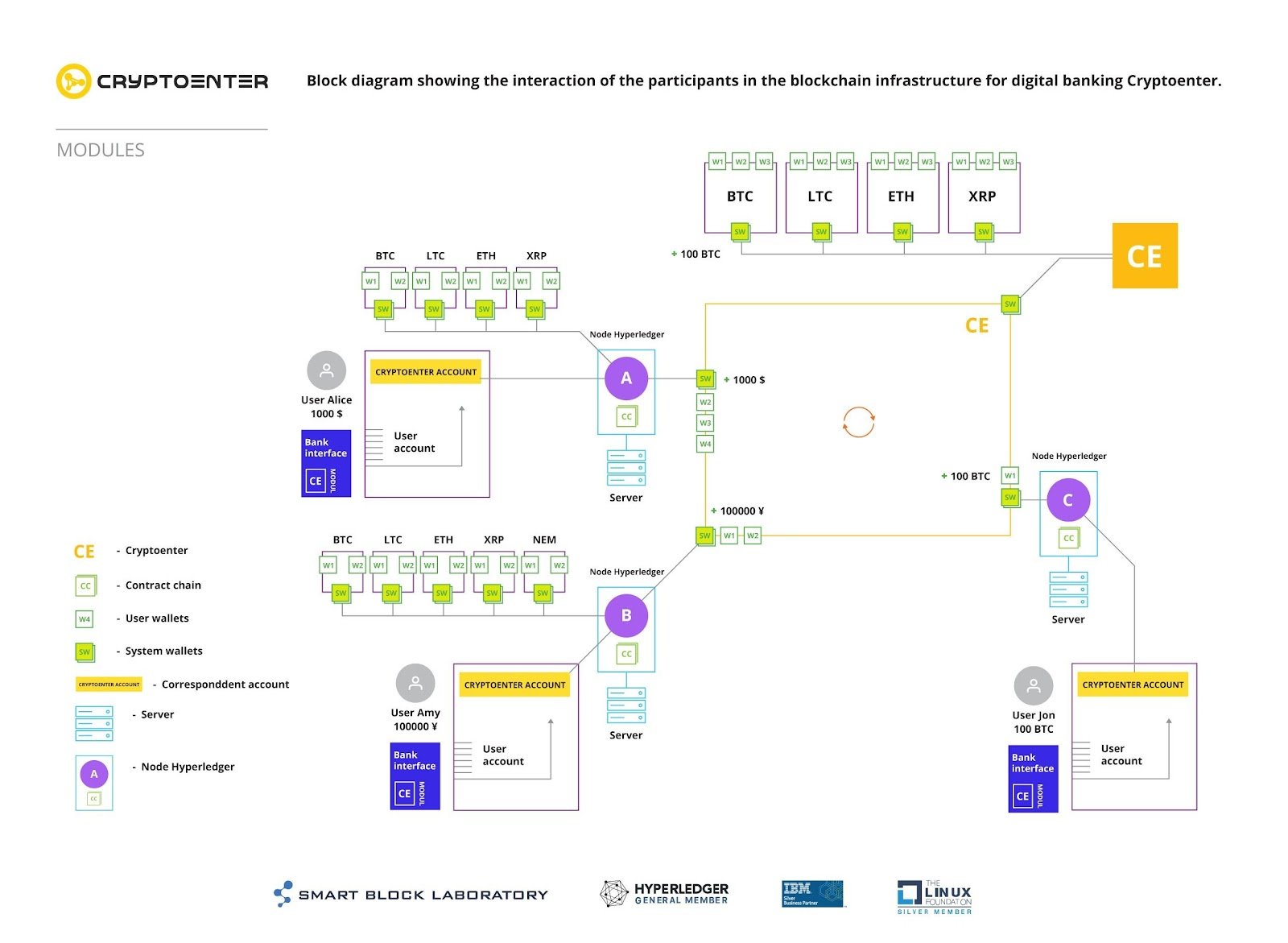

The following diagram shows the interactions within the Cryptoenter infrastructure:

According to a recent report, banks spend 72% of their IT budget on maintaining existing systems. Cryptoenter allows any bank to implement a complete DeFi system for a fraction of that budget – and enjoy all the benefits of digital banking without any additional development.